1 Introduction

Achieving carbon neutrality requires transitions across all industries and sectors. In UK terms, ambitions and policies concerning ‘carbon neutrality’ are seen as achieving ‘net zero’. While definitions vary, the UK Government defines net zero in the Climate Change Act (2050 Target Amendment) passed into law in 2019, which committed to a 100% reduction of greenhouse gas emissions by 2050 compared with 1990 levels [1].

Decarbonising home energy consumption in the UK, and particularly home heating, involves a complex transition. For energy supply at the national level, this involves a switch from fossil fuel use to decarbonised electricity. In the homes themselves, it involves reducing energy consumption through efficiency improvements and encouraging a switch from fossil gas boilers used in 23 million homes to low carbon heating such as heat pumps [2].

This challenge is significant. The UK’s housing stock is one of the oldest [3] and least energy and carbon-efficient in Europe [4,5,6]. In 2021 less than 2% of homes were heated with low carbon sources and the uptake of energy efficiency interventions compared poorly to mainland Europe [7]. Furthermore, despite heat pump sales surging 38% across Europe in 2022, the UK ranked bottom of the league table for heat pumps sold per 1000 households and 11th for total sales [8]. Despite this poor relative performance, urgency to address this challenge is growing in the UK. As people have witnessed and experienced the impacts of climate change and endured markedly higher energy prices since 2021 [9,10], calls for solutions have grown louder.

The UK’s Net Zero Strategy [11] and Heat and Buildings Strategy [12] as well as the International Energy Agency’s 10-Point Plan to Reduce the European Union’s Reliance on Russian Natural Gas [13], have spelled out that heat pumps would be the dominant technology to replace fossil gas boilers alongside energy efficiency upgrades to homes.

Heat pumps are a technology that use thermal energy found in the air, ground or water to circulate heat around homes. Critically, heat pumps can achieve higher levels of efficiency compared to both fossil gas boilers and other low carbon heat sources powered by renewable electricity, rather than fossil fuels.

To incentivise the transition towards heat pumps the UK Government introduced the Boiler Upgrade Scheme in 2022 [14], comprising a grant to homeowners to install heat pumps. The scheme aims to bolster the UK’s heat pump industry to achieve 600,000 heat pump installations per year by 2028 and 1.7 million per year by 2036, the current level of gas boiler installations (ibid).

However, this transition is not straightforward. Scaling up heat pump installations requires actions and investments by the Government, industry and homeowners. The process of switching a home from a fossil gas boiler-based heating system to a lower carbon, heat pump-based heating system can require spending money on home improvements to make the home heat pump-ready.

The aim of this research is to understand the extent to which the UK, or more specifically, industry and homeowners in England, are ready to scale and adopt heat pumps as a mainstream alternative to fossil gas boiler-based heating systems. Although much of the policy and industry context explored is UK-wide, this study focuses on England due to data availability and the devolved nature of key policy measures—notably the Boiler Upgrade Scheme. To investigate this, the research covers three areas. First, analysis combining two national datasets has been used to estimate the eligibility of the housing stock for the Boiler Upgrade Scheme and the readiness of that housing stock for heat pumps. Second, semi-structured interviews with senior managers in heat pump installation companies have been conducted to understand the challenges involved in increasing heat pump installations. Third, a nationally representative survey of homeowners in England has been carried out to understand their considerations around transitioning to low carbon heating systems.

1.1 Literature review

The literature review examines three areas. Section one looks at the UK’s energy market context and the overall approach taken to regulating energy. Section two focuses on the energy efficiency of the housing stock and the policies and incentives used to promote improvements. Section three reviews the differences between fossil gas boilers and heat pumps along with the policies and incentives used to encourage adoption.

1.2 Principles guiding the UK energy market

1.2.1 UK energy market context

The core principles of the UK’s domestic energy policy stem from a process of market liberalisation and privatisation of state-controlled energy companies started during Margaret Thatcher’s premiership and Conservative government in the 1980s. This period saw the Government pull back from directly controlling energy markets—by disbanding the Department of Energy, for example - and shift towards private companies competing in regulated markets.

This process of liberalisation continued throughout the 1990s and 2000s [15] with support from the Labour government elected in 1997 who maintained a focus on competitive energy markets. This included the Competition Act 1998 [16] which brought in the Competition Commission (now called the Competition and Markets Authority), and the Utilities Act 2000 [17]. The latter created a licensing system for energy supply companies, administered by the Gas and Electricity Markets Authority and regulated by the Office for Gas and Electricity Markets (“Ofgem”) with the Gas and Electricity Consumer Council (known as EnergyWatch) to protect consumer interests.

Competition was promoted by giving consumers greater choice. In 1999 homes were able to switch their energy supplier for the first time. The idea was to encourage energy providers to make efficiencies and compete for customers on prices and service quality. By 2002, following a period of consolidation, the 15 monopoly energy supply companies became the ‘Big Six’. Despite the benefits of greater competition [18], Ofgem’s energy supply probe in 2008 found that many consumers - particularly those in vulnerable groups—were not yet benefitting from competitive markets [19]. Despite this, Ofgem “remained convinced that consumers benefit most from a vibrant competitive market” [19].

In 2010 Ofgem launched a Retail Market Review which reported in 2011 [20] that 75% of consumers were on expensive, default evergreen tariffs.1(1 An evergreen tariff is a contract that automatically renews or ‘rolls over’ if the customer does not serve notice within the time stipulated by their current supplier.) The review claimed that consumers lacked obvious opportunities for engagement with the market, that energy prices tended to rise in response to wholesale cost increases but fall slower with decreases, and that significant market barriers made it hard for new companies to enter and compete in the market (ibid).

Despite growing evidence that the UK’s competitive energy markets were struggling to yield positive outcomes for customers, the Coalition Government of 2010-2015 again used legislation to promote competition and choice in the hope of improving outcomes for consumers. The Energy Act 2013 did this by giving Ofgem greater powers to force energy supply companies to offer their most affordable tariffs to consumers. However, in 2016 the Competition and Markets Authority found energy supply companies to be overcharging consumers by as much as £1.7 billion per year [21]. In response, the Competition and Markets Authority proposed a price cap, initially suggested for customers on prepayment meters (ibid). This was eventually introduced in 2019 for all customers [22].

1.2.2 Competition, choice and home heating

The overall focus by successive UK governments and Ofgem on policies that promote competition and consumer choice has also been reflected in legislation to improve the energy efficiency of the housing stock and encourage low carbon heating.

The Energy White Paper 2003 entitled ‘Our energy future—creating a low carbon economy’ outlined for the first time the requirement to limit carbon dioxide and committed the UK to work towards a 60% reduction in CO2 emissions by 2050 [23]. The paper was based on four pillars: the environment, energy reliability, affordable energy for the poorest, and competitive markets for companies, industries and households (ibid). It outlined a commitment to tackling the problem of “old, poorly insulated, draughty homes, where much spending on energy is simply wasted” and a goal to ensure every home is adequately and affordably heated (ibid). Similarly, it acknowledged that future energy policy and goals would be underpinned by several principles including reduced energy use, more renewable energy supply and preferencing market instruments and/or voluntary mechanisms over regulations if viable (ibid).

The Energy White Paper 2007 entitled, ‘Meeting the Energy Challenge’, was guided by similar principles [24]. For housing, the Government emphasised the importance of energy efficiency, better information for consumers, and appropriate incentives and regulation to encourage each home to reach its cost-effective energy efficiency potential, while also recommending a requirement for all new homes to be zero-carbon from 2016 (this commitment was then dropped by the Conservative Government in 2015).

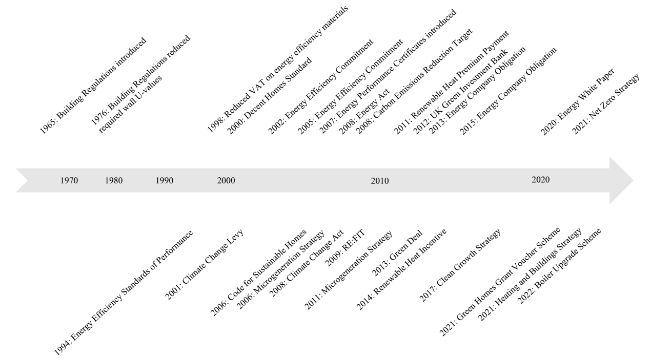

From 1965 to the present day, the UK has brought forward more than 50 policies, schemes and strategies to support the transition to a more energy efficient housing stock, including those illustrated in Fig. 1:

Kern et al. [26] proposed that these measures have generated a complex, fragmented policy environment for homeowners and companies, which has failed to encourage sufficient improvements in the housing stock [30]. One notable exception is the Carbon Emissions Reduction Target scheme 2008-2012, which encouraged the deployment of insulation and other energy efficiency measures in homes and exceeded its target [28]. This is discussed further in the next section. Kivimaa and Martiskainen [31] contend that without specific policies to push for greater energy efficiency - whether through new build or retrofit—it will be difficult to encourage the decarbonisation of housing. This suggests that it is not a lack of policies and incentives that stands in the way of decarbonising the housing stock, but implementing the right policies both individually and in combination.

1.3 Energy efficiency

Vine [32], Saidur [33] and Killip [34] show that increasing the energy efficiency of homes (with interventions such as insulation) is one of the most cost-effective ways of reducing carbon emissions. In the UK, increasing the energy efficiency of homes has also been linked with improved home valuations [35]. Who has delivered energy efficiency measures reflects the complexity of the UK competitive energy market and the focus on home ownership. Policies that place requirements on homeowners can be politically unpopular so the approach has often been to place the obligation on energy supply companies to complete the work themselves, or by using networks of local and regional contractors and subcontractors [36]. How this has worked in Government-legislated schemes such as the Carbon Emissions Reduction Target and Energy Company Obligation and Government-funded schemes such as the Green Homes Grant Voucher Scheme is discussed in the Sect. 2.2.3.

This section reviews the current energy efficiency of the UK’s housing stock and the role this plays in determining energy demand and consumption for heating. The role and sufficiency of building regulations and Government incentive programmes are then explored.

1.4 State of the housing stock

Research suggests that the residential sector accounts for 17% of global greenhouse gas emissions [37], 25.4% of EU-wide emissions [38] and 20% of UK emissions [7,39]. The UK housing stock is one of the least energy- and carbon-efficient in Europe [5], Commission for Climate Change 2019, with heating in homes accounting for 17% of the UK’s carbon emissions (Department for Business, Energy, and Industry Strategy 2019. Of the UK’s 24 million homes, studies show approximately 50% have an Energy Performance Certificate (“EPC”) rating of D2(2 Energy Performance Certificates rate homes according to their energy efficiency and are banded A-G (A being most energy efficient).) and 21% have a rating of E or worse [7]. Despite the energy efficiency of homes improving between 2001 and 2020, according to the Department for Levelling Up, Housing and Communities (2021), the rate of energy efficiency improvements to homes has to increase seven-fold for the UK’s housing stock to be EPC Band C or above by 2035 [40] - a vital task if energy use in homes is to be reduced and net zero achieved. This lack of progress is a concern because as Horne et al. 41], Morrissey and Horne [42], Moore [43], Fuerst et al. [35] reflect, the UK has one of the oldest housing stocks in Europe. To illustrate why this is an issue, Lowe and Chiu [44] point out that more than half of the UK’s homes were built prior to the introduction of building regulations in 1965, which for the first time required homes to have a basic level of thermal insulation. As Butt et al. [45] show, 20% of the UK’s homes are more than 100 years old and there is an annual replacement rate of approximately 1%. Secondly, 31% of the UK housing stock are solid wall properties, making them difficult and costly to insulate [46].

1.5 Building regulations

One way of influencing the energy efficiency of homes is through building regulations. Today, Building Regulations 2022 govern the construction and/or renovation of domestic buildings (HM Government 2022). Governments have also used building regulations and other standards to influence the energy efficiency of new homes. In 2006 the Labour Government consulted on an ambition for all new homes to be built to zero carbon standards from 2016. The Coalition Government then committed to this in the 2013 Budget [47]. This would have introduced a zero-carbon homes standard into building regulations, but the commitment was dropped in October 2015 to encourage house building by limiting costs and bureaucracy [48].

Changes to the Building Regulations in 2006, following the direction of the 2003 Energy White Paper [49], tightened energy efficiency requirements. For the first time, existing homes were given a score based on their energy efficiency using the Standard Assessment Procedure3(3 The Standard Assessment Procedure (SAP) is the methodology used by the government to assess and compare the energy and environmental performance of homes. SAP scores are used for EPC ratings.) (referred to throughout as “SAP”) [50]. Part L of the UK’s building regulations deals with the conservation of energy and sets standards dictating how materials and technology can be used to enable greater energy efficiency. This covers the insulation values of building materials, allowable area of windows, doors and openings, air permeability of the structure, the heating efficiency of boilers, the controls for heating appliances and systems, hot water storage and lighting efficiency.

The literature illustrates the issues that have arisen in the implementation of building regulations. According to Bell, Smith and Palmer [51], Part L of the 2006 Building Regulations failed to drive decarbonisation of the housing stock because of added complexity and uncertainty. Furthermore, Pan and Garmston [52] found that Part L1A of the 2006 Building Regulations only had 35% compliance. Littlewood and Smallwood [53] found that the purpose of building regulations was being undermined by limitations in the verification of construction processes.

While the energy efficiency of new buildings has improved since the 1970s, Kilip [34] highlights that these benefits have been undermined by growing energy consumption and changing demographics. Were these issues to be resolved, the use of building regulations to drive energy efficiency in the housing stock could be an important counterbalance. Indeed, in a critical assessment of building regulation effectiveness, Lingard [7] found that a whole house retrofit of an average home to become in line with 2010 Building Regulations would reduce heating demand and emissions by 65%. Moreover, if homeowners undertook measures that went beyond the 2010 Building Regulations, they could reduce carbon emissions from their home by 80% (ibid).

1.6 Policies promoting domestic energy efficiency

Outside of building regulations, the government has intervened in the market with incentives to encourage building fabric improvements. Of note are the Carbon Emissions Reduction Target scheme which started in 2008 and then the Energy Company Obligation and Green Homes Grant Voucher Scheme, which started in 2013 and 2020 respectively.

1.7 Carbon emissions reduction target

Introduced in 2008 following the end of the Energy Efficiency Commitment [54], the Carbon Emissions Reduction Target scheme required major energy supply companies to achieve targets - relative to their size—for reducing carbon emissions from domestic homes in the UK [28]. Set a target of saving 293 million lifetime tonnes of carbon dioxide (Mt CO2) by the end of 2012, the energy supply companies went further, achieving savings of 296.9 Mt CO2.

An independent report commissioned by the Department of Energy and Climate Change (2014) found a number of positive attributes about the first phase of the scheme running 2008-2011. These included a flexible means of delivery and breadth of scope, straightforward scoring of CO2 savings, simple administrative system, ability to support high volumes of measures at the lowest cost and a scheme seen as evolving from the previous supplier obligation scheme. Drawbacks included limited mechanisms to distribute the carbon savings to the most vulnerable, a lack of equity in supporting hard-to-treat homes and the private rented sector (ibid), encouraging energy supplier activity rather than consumer interest [55] and not targeting the full extent of private and social homes [56]. The CERT extension running 2011-2012 was successful in supporting the growth of the insulation industry, but more prescriptive in its scope and timescales which contributed to higher costs (Department of Energy and Climate Change 2014). After 2012, the scheme was replaced by the Energy Company Obligation.

1.8 Energy company obligation

Iterations of the Energy Company Obligation have been running since April 2013 and it mandates energy supply companies to promote and fund measures which improve the ability of low income, fuel poor and vulnerable households to heat their homes and reduce their heating demand through energy efficiency interventions [57,58].

According to literature and data, the Energy Company Obligation has been unsuccessful. A House of Commons Library report on the Energy Company Obligation noted that the scheme delivered just 2.7 million measures in 2 million homes compared to more than 8.5 million measures through the Carbon Emission Reduction Target and Community Energy Saving Programme [59]. The UK’s Climate Change Committee [4] remarked that the Energy Company Obligation had failed to drive uptake in energy efficiency in existing homes, noting that installations of loft and wall insulation in the UK were at just 5% of peak rate of installations in 2012 under CERT, despite significant market potential. Blacklaws et al. [60] reported after the first year of implementation that the Energy Company Obligation was complex and bureaucratic compared to previous schemes. This increased delivery costs, made it expensive and impeded take-up. The UK’s National Audit Office’s 2016 report on the scheme’s first phase noted that the Energy Company Obligation failed to deliver cost-effective carbon reduction compared to previous schemes and pointed out that the focus on hard-to-treat properties meant it was difficult for the supply chain to maintain scale [61]. Miu et al. [62] note that the scheme achieved less total carbon emissions reductions than previous schemes, failed to deliver its target for improvements to solid wall properties and was less cost-effective than expected. Katris and Turner [63] highlighted that the Energy Company Obligation had significant administrative and implementation costs that diverted funding away from retrofitting activities.

1.9 Green homes grant voucher scheme

The Green Homes Grant Voucher Scheme was introduced in July 2020 by the UK Government as part of a wider economic support package in response to the Covid-19 pandemic. The Green Homes Grant Voucher Scheme issued vouchers for two thirds of the cost of eligible primary energy efficiency measures such as solid wall, cavity wall and under-floor insulation and eligible secondary measures such as draught proofing, windows and doors, and smart heating controls [64]. Initially due to last until the end of March 2021, the Government announced it would be extended until the end of March 2022. Despite this extension, it suffered from a slow rollout amid claims that vouchers were difficult to apply for and a general reluctance by homeowners to have tradespeople in their homes during the pandemic [65]. While the academic literature is limited due to its recency, it joined the list of unsuccessful government-backed schemes in this area and was closed at the end of March 2021. According to the National Audit Office [66], the scheme helped upgrade just short of 50,000 homes at a cost of £314 million but with a rushed delivery schedule and administrative issues, the scheme caused frustration for both homeowners and installation companies.

In summary, the literature reveals an ageing housing stock in the UK that is difficult and expensive to retrofit, that Governments have struggled to update and enforce building regulations to drive energy efficiency for existing and new homes, and that specific schemes and incentives - notably the Energy Company Obligation and Green Homes Grant Voucher Scheme—have proven cost-ineffective and bureaucratic to deliver. Given these findings, this research will aim to examine and understand from heat pump installation companies which types of policy measures and incentives may be most effective at encouraging the retrofitting of homes to be heat pump-ready. It will also aim to understand the types of home improvements homeowners will consider and how much they would be willing to spend to make their homes heat pump-ready.

1.10 Heat technology choice

This section explores the predominant choice of replacement technology for gas boilers - heat pumps. The role and sufficiency of UK Government incentive programmes are then examined.

1.11 Heat pumps versus gas boilers

The current UK Government has referred to heat pumps as a long-term solution to providing low-carbon heat in homes [12]. The Heat and Buildings Strategy 2021 made a number of commitments: first, that all new homes from 2025 are to be net zero-ready and built using heat pumps rather than natural gas boilers; second, expanding the capacity and capability of the UK market to deploy at least 600,000 heat pumps per year by 2028; and third, to phase out natural gas boilers completely by 2036, requiring approximately 1.7 million heat pump installations per year by the same year.

A heat pump is an efficient alternative to a gas boiler-based heating system. Rather than directly burning fossil fuels to generate heat, they extract ambient heat from the air, ground or water to heat buildings. The most common type in the UK are air source heat pumps, which operate by drawing heat from outside air through a system of coils holding a refrigerant fluid with a very low boiling point. This absorbs the heat at a lower temperature. The refrigerant is then pressurised and heat is transferred to water that circulates around a home’s radiators [67]. The literature shows that heat pumps will provide an immense contribution to a low carbon future [68], with wide evidence from Switzerland, France, Italy, Germany and Denmark illustrating they are among the most cost-effective and energy-efficient systems for housing with sufficient building standards [69,70,71]. Furthermore, according to analysis by Gibb et al. [72] of performance of 550 domestic heat pump systems in both mild cold climates and extreme cold climates in Europe, North America and China, heat pumps were shown to provide the most efficient heating when compared to alternative fossil fuel and electric resistive heating systems. However, while heat pumps are appealing and more efficient alternatives to gas boilers, they are different and not one-for-one swaps. Cost, the readiness of homes, and how homeowners use their systems all impact the perceived suitability of heat pumps for use in heating homes.

An area for concern is the manner in which heat pumps are being presented to the market, and what makes them perform well. For example, the UK Government’s Boiler Upgrade Scheme - that is discussed in detail later—promotes heat pump installations through the form of a subsidy paid upfront. This focus on the heat pump and not the related works that make a home ‘heat pump-ready’ risks creating the perception that heat pumps are interchangeable with boilers.

Academic literature and industry studies are starting to suggest that care is needed to avoid setting the wrong perceptions. How well homes retain heat - illustrated by the U-values4(4 U-Values are a measure of how effective elements of a building’s fabric are as insulators. The lower the U-Value, the slower heat is able to transmit through it, and so performs better as an insulator [73].) of key materials used for insulation—and the quality of a heat pump system’s design, installation, and operation, all impact the performance of heat pumps in homes. In an early field trial between 2008 and 2013, many of the heat pumps monitored did not perform as expected in their initial phase of use [74]. However, after a range of interventions 62.5% of installations achieved improved performance in the second phase (ibid). Underpinning performance in both phases was the effectiveness of the design, installation, and commissioning of the heat pumps (ibid). Heinen et al. [75] adds that heat pumps normally operate at reduced capacity because of poor system design, faulty installations and weather fluctuations. In a review of literature on heat pump field trials, Carroll et al. [76] reveal that heat pumps are only efficient in well insulated buildings and the role of users is important in efficiently operating the technology too. Furthermore, Abbasi et al. [77] argue that heat pumps cannot serve as a standalone substitute for gas boilers, citing the necessity of upgrades to buildings and the electricity system.

The literature identifies a number of issues connecting higher costs with poor uptake. Gaur et al. [68] highlight the price ratio between alternative energy sources and electricity, investment costs and installation costs as major barriers to heat pump uptake in Europe. Similarly, Wang et al. [71] highlight that heat pumps with significant capital and installation costs can have limited running cost benefits compared to gas boilers. According to Bhattacharya [78], heat pumps can cost three times more than a gas boiler to install. To work efficiently homes can require a range of upgrades in preparation: a survey of heat pump installation companies by the Heat Pump Association [79] found that 75% of homes required at least some upgrades to radiators, and therefore additional cost, for heat pumps to operate at optimal efficiency in the home. Higher costs for early adopters of new technologies are to be expected but a path to more affordable costs is needed for wide-scale adoption.

The UK’s market structure for the delivery and installation of gas boilers and now low carbon heating has typically been small and medium sized installation companies operating at a local and regional level. According to MCS, the accreditation body for heat pump installations, there are 1061 heat pump installation companies registered for the Government’s Boiler Upgrade Scheme [80]. The historical focus on specialist, local, small and medium sized enterprises has recently started to change though larger, nationally spread energy supplier companies joining the heat pump installation market [81]. As with energy efficiency improvements discussed earlier, the heat pumps installation market is impacted by Government policy and incentives (discussed in the next section). In recent years, the most significant regulatory interventions with wide remits to incentivise both energy efficiency measures and low carbon heating installations have been the Renewable Heat Incentive, Green Deal and Boiler Upgrade Scheme - the latter being a focus of this study.

Regarding technology adoption, researchers have considered the balance consumers perceive between costs and benefits when replacing a boiler with a heat pump. In early work, consumer awareness about renewable heating systems was low [82,83,84]. Furthermore, middle aged, highly educated, higher earners were seen to have a higher chance of knowing about and choosing renewable heating systems such as heat pumps [82,83,85]. More recently, Williams et al. [86] found that 58% of survey respondents had heard of heat pumps, but 76% of respondents in a survey by Addario et al. [87] had either not heard of or knew nothing about heat pumps. Philips and Seaford [88] conducted a survey of the British public and found that 77% supported an ambitious approach to heating with the Government playing a role. Hafner et al. [89] in a behavioural study exploring the role of normative, financial and environmental information in promoting the uptake of energy efficient technologies, found that people were willing to consider energy efficient technologies such as heat pumps, but this willingness reduces when cost factors are considered.

In summary, there are financial, industry and behavioural obstacles which need to be overcome to making a successful transition from gas boilers to heat pumps. This research aims to understand the scale of these challenges through analysis of the proportion of homes that are heat pump-ready, and by understanding the opinions of heat pump installation companies and homeowners.

1.12 Policies promoting domestic low carbon heat technology adoption

The UK government has intervened in the market to encourage the uptake of domestic low carbon heat technologies. Most significantly through the Green Deal in 2013, then Renewable Heat Incentive in 2015 and Boiler Upgrade Scheme in 2022. These schemes have aimed to incentivise homeowners to invest in low carbon heating technologies for their home, while encouraging the development of an industry and workforce.

1.13 Green deal

Introduced in 2013 by the then Department of Energy and Climate Change, the Green Deal was a framework to enable companies to offer consumers energy efficiency improvements to their homes and/or low carbon heating at no upfront cost before recouping payments through instalment-based charges on their energy bills [61]. The Green Deal’s ‘golden rule’ was for the expected financial savings to be equal or greater than the costs attached to the energy bill. Aligned with the principles of wider energy policy discussed earlier, the Green Deal was a market mechanism aimed at consumers rather than a regulated requirement placed on energy supply companies, continuing the Government’s commitment towards giving consumers choice in energy markets [55]. However, despite expecting to deliver millions of energy efficiency savings packages through the Green Deal [90], by the end of 2015 just 20,346 energy efficiency measures had been installed using Green Deal finance [91]. In 2015 the new Conservative Government ended funding for the Green Deal, with Eyre and Rosenow [92] calling it the biggest failure in the history of UK energy policy.

The Green Deal did not succeed for several reasons. First, it had limited financial appeal [93]. Marchand et al. [92,94], Howarth and Roberts [95] highlighted how the higher cost of borrowing through Green Deal finance compared to typical borrowing rates put homeowners off. Chryssochoidus et al. [96] found that homeowner intentions towards energy efficiency improvements were weakened by uncertain financial benefits. Second and linked to the cost of borrowing, was that certain measures - such as biomass boilers and draught proofing - were not expected to meet the Green Deal’s “golden rule”5(5 Known as the “golden rule” of the Green Deal, the expected financial savings must be equal to or greater than the costs of delivering the measure (Department of Energy and Climate Change 2010).) because the expected energy savings were less than the cost of implementing them [92,97]. As a result, the Green Deal was only able to provide tangible support to homes with the worst energy performance [93]. Third, low awareness [94] and insufficient consumer engagement [92,95] also held the scheme back.

1.14 Renewable heat incentive

The Renewable Heat Incentive aimed to encourage energy efficient, low-carbon heating in the UK. Introduced in 2014 for domestic homes, the incentive replaced the Low Carbon Buildings Programme, the capital grant-based support scheme closed in 2010 [98]. The Renewable Heat Incentive was designed to offset a homeowner’s costs of installing renewable energy systems to heat their homes, such as heat pumps, biomass boilers, and solar water heating [99]. Government projections expected 12% of heating in the UK to come from renewable sources by 2020 as a result of the policy (Department for Energy and Climate Change 2011a). In 2018, the UK Government’s Public Accounts Committee presented evidence that this was unlikely to be achieved [99] and the Renewable Heat Incentive was replaced by the Boiler Upgrade Scheme in April 2022.

The literature demonstrates a mixture of opinions on the Renewable Heat Incentive. Connor et al. [100] argue that the Renewable Heat Incentive put the UK at the forefront of efforts to promote renewable energy sourced heat. In a review of the potential value of the Renewable Heat Incentive for promoting solar thermal heat, Abu-Bakar et al. [101] found that the Renewable Heat Incentive could drive significant adoption of solar thermal systems in the UK, depending on location, but cautioned that the scheme was likely to be ineffective because the payment period was too short and the payments too low [102].

Prior to launching the Renewable Heat Incentive, Bergman [103] had warned that issues such as technical problems and low-quality installations, institutional issues, poor information supply to users and improper use could delay or jeopardise plans for rolling out renewable microgenerators such as heat pumps. The literature assessing the Renewable Heat Incentive with respect to heat pump adoption found that low uptake was largely down to non-financial barriers such as process issues (for example, the need for an in home assessment) performance requirements (heat emitter size) [104] and the hassle of installation [105].

When the scheme ended in March 2022 it had not met its own expectations for installations [106]. Furthermore, the scheme failed to stimulate the industry’s workforce. Between 2015 and 2019, the total number of heat pump installers reduced before recovering between 2020 and 2022 (ibid). Those that did benefit from the scheme reported high levels of satisfaction with their systems after the first year, and increased satisfaction after two years (ibid).

1.15 Boiler Upgrade Scheme

The UK’s Boiler Upgrade Scheme is the focus of this study and was launched in April 2022. Unlike schemes offering financial returns over time, the scheme provides up front grants to subsidise the installation of heat pumps: initially £5,000 for Air Source Heat Pumps and £6,000 for Ground Source Heat Pumps, and from October 2023 this was uplifted to £7,500 for both respectively [107,108]. So far, the scheme has not accelerated adoption to levels seen elsewhere in Europe, with the UK’s adoption curve still lagging behind countries such as France, Germany, Netherlands and Poland [8]. In the scheme’s first year—running between 23 May 2022 and 31 March 2023—a total of 9,983 Boiler Upgrade Scheme grant payments were approved and paid [109]. As a recently introduced scheme, there is limited evaluation though the House of Lords Environment and Climate Change Committee in February 2023 [110] suggested that the scheme was not on track to deliver 90,000 grants by the end of 2025, when the scheme was due to close. Subsequently the scheme has been extended to 2028 [108]. Separate from the Boiler Upgrade Scheme, the UK’s sales tax (VAT) was reduced from 5 to 0% for contractors installing energy saving materials (insultation, draught stripping) or grant-funded heating equipment (air source heat pumps, ground source heat pumps) [111].

In summary, literature on policies promoting domestic low carbon heat technologies in the UK suggest that both the Green Deal and Renewable Heat Incentive received some praise but did not succeed in transitioning significant levels of homeowners to low-carbon heating. Their weighting was towards market-based financial mechanisms spread over the lifetime of an installation. They did not overcome the barrier of upfront costs and overlooked non-financial factors in the customer journey such as the need for assessments, performance requirements and disruption. The 2022 Boiler Upgrade Scheme provides upfront grants but early indications are that it has achieved a slower rate of uptake than hoped [112].

1.16 Outlook

Previous studies have illustrated the challenges of instilling greater fairness in energy markets through market-led approaches that incentivise competition and choice while also encouraging energy efficiency and low carbon heating [19,20,21]. Indeed, although the quantity of policies, programmes, and incentives pursued illustrate the UK Government’s keenness to steer energy markets, these efforts have created complexity [26] and often failed to deliver the desired outcomes [30].

To this end, efforts to improve the energy efficiency of the housing stock through building regulations and policies have not made a meaningful difference [4,51,52,53,58,66]. Building regulations have not succeeded due to issues such as complexity and uncertainty [51], low compliance [52], and poor verification processes [53]. Considering policies and incentives, the Energy Companies Obligation has struggled to deliver its aims because of bureaucratic complexity [60], its limited scope to certain buildings [61], and being cost-ineffective [62,63].

Finally, studies also highlighted considerations around switching from fossil gas boilers to heat pumps, and efforts made by the UK Government to promote low carbon heat options such as heat pumps. Considering the use of heat pumps rather than fossil gas boilers, studies emphasised the need for home improvements to make homes more energy efficient and the need for well-designed heat pump systems if good heat pump performance is to be achieved [69,70,71,76,77]. Studies also expose the difficulties in devising effective policies and incentives to encourage the adoption of low carbon heating technologies [91,92,93,94,95]. In particular, we’ve seen that market-based interventions with a high cost of borrowing [91] or that require homeowners to cover significant upfront costs [99] have not adequately catalysed growth of the heat pump market. Furthermore, it is unclear how industry will help the majority of homeowners - beyond the minority of middle-aged, wealthier and more educated homeowners who are more likely - and able—to adopt low carbon energy solutions in their homes [82,83,85].

This study aims to add to our understanding in several ways. Firstly, by estimating the proportion of the private housing stock that are eligible for the Boiler Upgrade Scheme and that are heat pump-ready. Secondly, if homeowners are to make the home improvements necessary to make their homes heat pump-ready, this study explores what these improvements entail, their cost, and the attitudes of installers and homeowners to completing the improvements necessary. In doing so, this study explores the readiness of industry to deliver the works needed for homes to be heat pump-ready and successfully install heat pumps. It also investigates the suitability of the Boiler Upgrade Scheme to meaningfully encourage homeowners to adopt heat pumps and hit their targets.

1.17 Methodology and method design

This chapter outlines the methods used for research, the rationale and limitations for each method, how data was selected, collected and analysed. Three research methods have been used:

1.18 Data analysis to estimate Boiler Upgrade Scheme-eligibility and heat pump-readiness

This analysis uses two publicly available datasets to estimate the proportion of English homes that are eligible for the Boiler Upgrade Scheme, and separately, ready for a heat pump. The two datasets used are as follows:

● English Housing Survey data, which collects information about people’s housing circumstances together with the condition and energy efficiency of homes. It contains 19.8 million owner occupied homes [113].

● Energy Performance Certificate (EPC) data, which records a measure of the energy efficiency of homes in England (and Wales) and contains 20.8 million existing owner-occupied homes [114].

The results of this analysis, alongside insights from the literature review, then inform the subsequent methods: the questions for semi-structured interviews with heat pump installation companies and the survey of English homeowners.

1.18.1 Estimating the proportion of homes that are Boiler-Upgrade Scheme-eligible

The Government has set a clear eligibility criterion for the Boiler Upgrade Scheme [14]. This requires a home to have a valid Energy Performance Certificate (EPC) with no outstanding recommendations for loft insulation or cavity wall insulation.

While it is possible to evaluate an individual home’s eligibility for the Boiler Upgrade Scheme by looking at its individual EPC certificate, this data is not aggregated at a national level to specify the number of homes in each EPC Band (A-G) that do or do not have both wall insulation and loft insulation.

To produce an estimate for the proportion of homes in England considered eligible for the Boiler Upgrade Scheme, English Housing Survey data has been used because it provides aggregate data on the proportion of homes that have specific types of insulation, such as cavity wall, solid wall and loft insulation. However, it does not provide aggregate data for homes that have both cavity wall insulation and loft insulation, which is the requirement for the Boiler Upgrade Scheme. For this estimate it is assumed that all homes with full cavity or solid wall insulation also have loft insulation and are therefore eligible for the Boiler Upgrade Scheme. This assumption was then tested by selecting and reviewing a representative sample of individual EPC Band C properties with wall insulation to see if they also had loft insulation. For statistical significance, based on a population size of 7,041,114 EPC Band C homes in England, a sample size of 69 was needed6(6 Sample size calculated using Survey Monkey sampling tool (accessed here: www.surveymonkey.co.uk/market-research/resources/how-to-get-a-representative-sample/).) to achieve a confidence level of 90% with a 10% margin of error [114]. Data was selected proportionally according to the geographical distribution of EPC Band C homes using the UK Government’s Energy Performance of Buildings Dataset dashboard (https://epc.opendatacommunities.org) and published data on Domestic Properties by Region by Energy Efficiency Rating [114]. The results supported the assumption; 68 of the 69 selected Band C homes with wall insulation also had loft insulation.

1.19 Estimating the proportion of homes that are heat pump-ready

A heat pump can be installed and used to heat most, if not all, homes. Furthermore, the performance of an installed heat pump system is determined by the home’s capacity to retain heat (insulation and air-sealing) and the appropriateness of its pipework and heat exchangers (radiators) used to distribute heat [115]. Using the relevant industry standards and guidance, the characteristics in a home that contribute to higher or lower heat pump-readiness are listed in Table 1. The presence of these characteristics either increase or decrease system efficiency (often reflected in the system’s ‘Coefficient of Performance’7(7 Coefficient of Performance (CoP) is a measure of a heat pump’s efficiency. CoP indicates a ratio of useful heating or cooling produced by the unit against the energy it consumes. The higher the CoP, the more energy efficient and cost effective the heat pump is [115].)) and in turn, running costs.

| Heat pump-ready | Not heat pump-ready |

|---|---|

| Well insulated, air sealed and draught-proofed to mitigate heat loss For example: with cavity wall insulation or exterior wall insulation and loft insulation (with low/good U-values) | Poorly insulated, air sealed and draught proofed For example: Solid walls with no insulation and stone/concrete floors and no heat loss mitigation. Cavity walls with no or partial insulation and stone/concrete floors and no heat loss mitigation, e.g. through draught proofing |

| Good dispersal of heat through building: For example: underfloor heating, fan (forced draught) convector heating, high output low temperature radiators | Poor dispersal of heat through building: For example: traditional pipework and radiators, especially if performance has reduced over time |

| Double or triple glazed windows (with low U-Values) | Single glazed windows (with high U-Values) |

| System design and pipework sizing suitable for heat pump use. Newer systems are often ‘over-sized’ on installation and can deliver adequate heat when a boiler is replaced with a heat pump | Needs exceed the capacity of existing system and pipework |

In considering the level of heat pump-ready homes, it is important to differentiate between estimates that reflect Technological Readiness Level [117] and Market Readiness Level [118,119]. As an established technology, the technology readiness level of heat pumps is high and the technology readiness of actions to make homes heat pump-ready is also high - the requirements in Table 1 are also established technologies. In contrast, a market readiness level considers factors beyond the required technologies [119] such as here the readiness of the installation industry and the interest of customers in paying for home improvements. This leads to a range in estimates: the proportion of homes that can be estimated as heat pump-ready from a technical perspective (referred to as ‘technical readiness’) and the proportion of homes that are also heat pump-ready in terms of what may be acceptable to the consumer and suitable for heat pump installation companies (referred to as ‘market readiness’).

EPC data is used as the primary dataset to analyse heat pump-readiness because, despite its limitations in terms of aggregation to determine eligibility for the Boiler Upgrade Scheme, the ‘A-G’ categorisation does provide a valuable filter and proxy for what is either definitely heat pump-ready or definitely not heat pump-ready in the housing stock. A-B rated homes are assumed likely to be heat pump-ready based on when they were built and the standard they were built to. For the opposite reason D-G rated homes are assumed unlikely to be heat pump-ready. However, uncertainty remains over the proportion of Band C homes that meet technical readiness and market readiness.

In this method, the proportion of EPC Band C homes estimated not to meet market readiness is calculated using data from a Heat Pump Association survey of heat pump installation companies in 2021. According to the survey, 75% of heat pump installations require upgrades to radiators [79]. The survey has a good sample size relative to the industry’s size and has been conducted by one of the industry’s two trade bodies, the Heat Pump Association. The method therefore provides a larger estimate of technical readiness and a smaller estimate of market readiness. Whether this is an appropriate way to distinguish between technology- and market-readiness is then tested in the following two methods where the readiness of installers and homeowners are studied.

1.20 Semi-structured interviews with Senior Managers in heat pump installation companies

This involved semi-structured interviews conducted with 12 Senior Managers in heat pump installation companies to gauge their views on the readiness of UK housing stock for heat pumps. The interviews also discussed how their companies may adapt to meet market needs and the adequacy of government incentives and regulations.

The rationale for choosing this method was to get some objective and practical insights [120] and qualify assumptions made in other methods [121]. Limitations include the significant time required to set up and conduct interviews, write up transcripts and interpret findings (ibid), no guarantee of precise findings from a relatively small sample (ibid), and often losing the opportunity to understand how the subjects themselves articulate the topic [122].

Heat pump installation companies, as noted in Table 2 below, were selected using the directories of the Heat Pump Association, Heat Pump Federation and MCS, the standards organisation that certifies low-carbon and renewables products and installations. This enabled a selection of companies with different sizes and territorial focus. Over 100 heat pump installation companies (taken from the 1061 Boiler Upgrade Scheme-eligible companies) were contacted using a combination of direct emails to publicly available company email addresses and direct messages on LinkedIn, a professional networking website. Reflecting the fact that the majority of heat pump installations in the UK market in 2022 were delivered by small and medium sized companies, all interviews were held with senior employees working for companies with under 100 staff members.

Table 2 List of interviewees |

| Company number | Seniority of interviewee | Company employees (FTE) | Region | Focus |

|---|---|---|---|---|

| 1 | Director | 1 | Greater Southampton area | Heat pump installations |

| 2 | General Manager | 27 | Yorkshire and Humberside | Heat pump installations |

| 3 | Managing Director | 4 | Southwest England | Heat pump, air conditioning, solar PV installations |

| 4 | Managing Director | 35 | East of England | Heat pump and solar PV installations |

| 5 | Technical Director, Designer and Installer | 3 | Yorkshire and Humberside | Heat pump installations |

| 6 | Senior Consultant | 21 | Surrey | Consultancy on decarbonisation projects, including heat pump installations |

| 7 | Head of Air Source Heat Pumps | 16 | UK-wide | Heat pump installations |

| 8 | Director | 19 | Yorkshire and Humberside | Heat pump and solar PV installations |

| 9 | Business Leader / Co-founder | 65 | Gloucestershire | Heat pump installations |

| 10 | Managing Director | 9 | Greater Southampton area | Heat pump installer, EV charger installations |

| 11 | Director | 4 | Norfolk and Cornwall | Heating and plumbing, specialising in renewables installations |

| 12 | Director | 2 | Lincolnshire | Heat pump installations |

The interviews provided a mixture of qualitative and quantitative data and therefore a combination of methods have been used. Each interview was recorded, transcribed, and analysed. For the closed questions, answers have been collated, counted and compared. For the open-ended questions, which comprise the majority of the interview content, a Braun and Clarke (2006) thematic analysis has been conducted to draw out recurring themes, issues and barriers.

1.21 A nationally representative public opinion survey on heat pump adoption and readiness

This involved surveying homeowners about the transition to lower carbon heating, and the home improvements necessary to ensure homes are heat pump-ready. The rationale for choosing this approach was to gain a primary perspective from homeowners, who are central to the energy transition in question. With this perspective, it is possible to triangulate and test the managerial perspectives provided by heat pump installer companies and the estimation of the proportion of homes that are heat pump-ready to uncover unmet needs and thus identify opportunities for business model innovation. There are some limitations to this approach; the survey is only a snapshot in time of a market influenced by rapidly changing socio-economic forces.

The homeowner data was taken from a nationally representative survey of 2,000 British adults conducted online between 29 and 30th June 2022 by a market research company, JL Partners Ltd (www.jlpartners.co.uk), and commissioned by the Low Temperature Heat Recovery Network Technologies (LoT-NET), a UK Research & Innovation backed programme.8(8 The Low Temperature Heat Recovery Network Technologies (LoT-NET) programme is a research collaboration between Warwick Business School, The University of Warwick Engineering Department, Loughborough University, London South Bank University and Ulster University. LoT-NET is supported by UKRI and the EPSRC, award EP/R045496/1 (www.lot-net.org/).) To select homeowners in England with gas boilers, demographic and pre-qualification questions were asked. Specifically, the survey tests homeowner opinions on: likeliness (intention) to decarbonise their home’s heating system within five years; awareness of the types of home improvements necessary to make their home heat pump-ready; willingness to consider types of home improvements; understanding of whether their home meets the Boiler Upgrade Scheme’s eligibility criteria; willingness to spend money on home improvements to make their home heat pump-ready, and; level of concern of about aspects of transitioning their home to lower carbon heating. The survey also enables the testing of relationships between independent variables such as age or combined household income (“income”) and the dependent variables listed above. Moderated regressions were run on the impact of age on income and vice versa on several dependent variables, but they were not statistically significant.

Further, the sample was made representative by quotas being put on age, gender, region, socio-economic group that match census data, before weighting was applied so the final data matches the quotas. The literature review and data collected in previous research methods informed the questions. To produce nuanced insights, Likert style questions and response options have been used alongside some dichotomous-based (choice based) questions.

1.22 Results and analysis

1.22.1 Boiler upgrade scheme eligibility and heat pump-readiness

As noted in the previous section, the UK Government does not provide exact definitions or figures for the number of homes that are Boiler Upgrade Scheme-eligible and heat pump-ready. The purpose of this analysis is to estimate both values and so determine what gap might exist between the two. Also when homes are evaluated as heat pump-ready, there has also not been an analysis that considers the difference between the technical readiness of homes and a market readiness that also considers the perspective of installers and homeowners.

1.23 Estimating boiler upgrade scheme eligibility

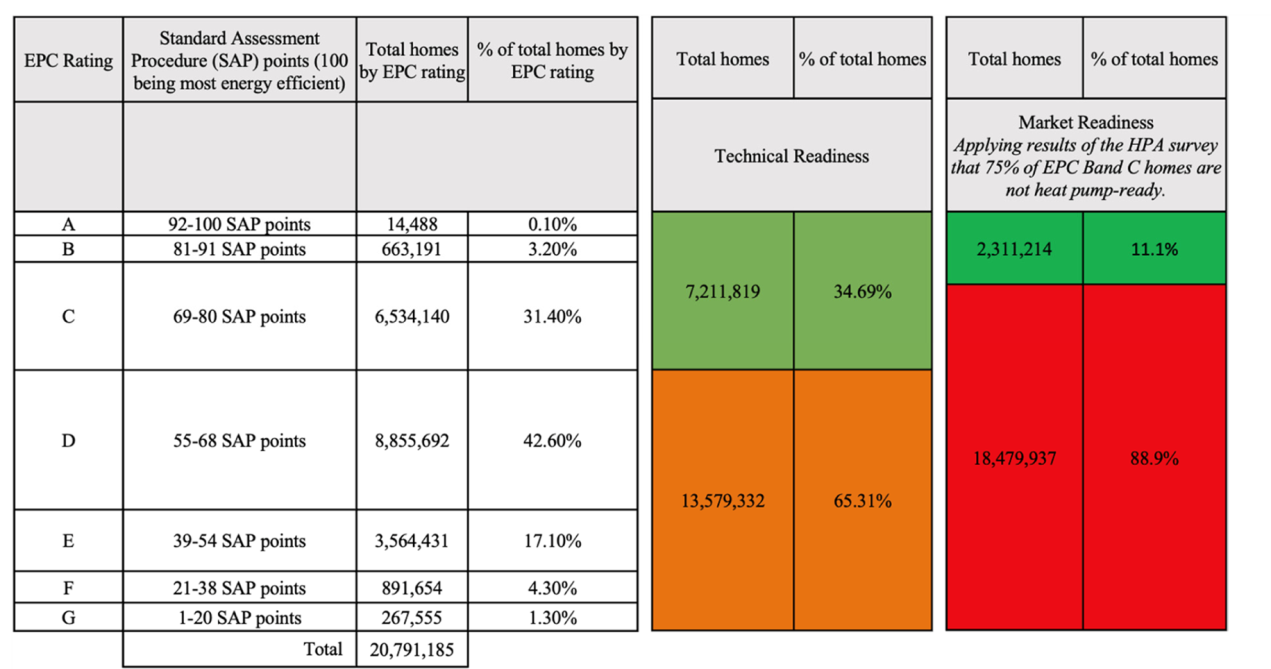

Using the English Housing Survey data-set and applying the assumption that all homes that have wall insulation also have loft insulation, we can see that 49.9% of the housing stock is estimated to be eligible for the Boiler Upgrade Scheme, as shown in Table 3.

Table 3 Percentage of private housing stock estimated to meet the Boiler Upgrade Scheme criteria for insulation (Analysis of data from English Housing Survey 2021 to 2022: headline report) |

| Total | |

|---|---|

| Cavity wall insulated | 9,337,000 |

| Solid wall insulated | 535,000 |

| Total insulated | 9,872,000 |

| Total stock | 19,780,000 |

| Percentage of private housing stock estimated to meet the Boiler Upgrade Scheme criteria for insulation | 49.9% |

1.23.1 Estimating heat pump-readiness

As described in Sect. 3.1, EPC data is used as the primary data-set to analyse the proportion of homes in England that are heat pump-ready in terms of technical readiness and market readiness. The results of this analysis are shown in Table 4.

Table 4 Estimates of heat pump-readiness in England in terms of technical readiness and market readiness (Analysis of data from Energy Performance Certificate data) |

|

If one assumes that all EPC Band C homes are heat pump-ready—where heat pumps and the typical home improvements are treated as established technologies—35% of the housing stock is estimated to meet technical readiness. However, if you consider the need for additional work such as new radiators and additional pipework, this estimation drops to 11%, which we propose is the market readiness level. In the next two sections, we provide evidence regarding whether installers and homeowners are ready to include such additional work and so whether the market readiness level is more reflective of reality than the technical readiness level.

A gap between technical- and market-readiness has been evident in guidance provided by the UK government regarding the Boiler Upgrade Scheme in the Heat Pump Ready Programme Questions document published by the UK Government in 2021 [123]. In reply to a question which stated that 80% of homes are not heat pump-ready as their U values are too high (a value reflecting the market readiness proposed here), the Government’s reply was that “80 to 90 per cent of homes currently have sufficient energy efficiency and internal electrical limits to accommodate a heat pump” (a value closer to technical readiness calculated here) (ibid).

Evaluating market readiness involves giving installers and homeowners a sense of the work involved beyond installing the heat pump and the cost of such work. Table 5 provides estimates for the costs of retrofit measures that can be necessary to achieve a heat pump-ready home. The costs outlined below are based on the Government’s most recently commissioned report from 2017, entitled ‘What Does it Cost to Retrofit Homes?’ [124]. Costs in that report have been inflation-adjusted to 2022 using the Bank of England’s Consumer Price Index-based inflation calculator. This approach offers the advantage of drawing values from a single, government-commissioned study but 2022 prices for certain measures from various sources have been included as additional reference points. The 2022 prices are generally similar which supports using the inflation-adjusted values from 2017 in further calculations.

Table 5 Cost of retrofit measures adapted from Palmer et al. 2017 and updated to reflect inflation |

| Retrofit measure | 2022 inflation adjusted unit costs - mean value taken from range [125] | 2022 inflation adjusted total cost (small semi-detached home (less than 80m2)) - mean value taken from range [125] | 2022 total cost estimates (semi-detached 3 or 4 bedroom home) - online prices [125] |

|---|---|---|---|

| Cavity Wall Insulation [126] | £7 per square metre of wall | £671 | £750—£1000 |

| Solid Wall Insulation [126] | |||

| Internal wall insulation | £115 per square metre of wall | £8,869 | £5000 - £7000 |

| External wall insulation | £139 per square metre of wall | £9,419 | £8500—£15,000 |

| Loft insulation [126] | |||

| Insulation installed at the joists | £18 per square metre | £465 | £550—£750 |

| Insulation at the rafters | £35 per square metre | £2,590 | n/a |

| Draught-proofing | £9 for 6 square metre of window film | n/a | n/a |

| £11 for 10 m of door or window seal | n/a | n/a | |

| £15 for a letterbox draught excluder | n/a | ||

| New radiators and pipework [127] | £300 per radiator (scope to be higher or lower depending on choice / existing radiator sizing) | ||

| Double or triple glazed windows [128] | n/a | £6,947 | UPVC: £3,000—£5,000 Hardwood: £5,000—£6,000 |

| Figures rounded to nearest £ | |||

1.24 Summary

There is a significant difference between the number of homes in England that are estimated to meet the Government’s criteria for the Boiler Upgrade Scheme (50%) and the number of homes in England that are heat pump-ready in terms of market readiness (11%) and technical readiness (35%). This phenomenon is referred to as the “eligibility-readiness gap”. Some gap is manageable - not all those eligible will apply. But a significant gap could create an obstacle to expanding heat pump adoption. To understand whether the market readiness level reflects reality more than the technical readiness level, the next two methods consider the view of installers and homeowners respectively.

1.25 Semi-structured interviews with heat pump installation companies

The second method involved 12 semi-structured interviews with heat pump installation companies. These interviews asked the participants to verify the data collected in the first method and then discussed the readiness of the English housing stock, how their companies will adjust to meet the needs of the growing market and their view on the actions of government in support of the market.

1.26 Perspectives on the readiness of the housing stock for heat pumps and cost implications

Respondents were first asked about the proportion of the English housing stock they thought was heat pump-ready. Two thirds of heat pump installation companies said no more than 10% was heat pump-ready. This was similar to the 11% estimated from EPC data in the previous section.

When asked about the suitability of the Government’s eligibility criteria for the Boiler Upgrade Scheme for selecting what they would determine to be heat pump-ready homes, five respondents said it would not be sufficient, four said it would, and three didn’t answer. Despite many heat pump installation companies saying the criteria are low in terms of energy efficiency requirements, the range of perspectives may indicate different working definitions of what constitutes heat pump-ready.

The interviewees were then asked to identify three measures from an exhaustive list of building upgrades (Additional file 1) which they feel contribute most to a home being heat pump-ready. ‘Cavity wall or solid wall insulation’ was the most picked retrofit action (selected by 92%) and the most listed in first place, followed by loft insulation (75%), then replacing radiators (50%). Air sealing/draught proofing followed in fourth (42%).

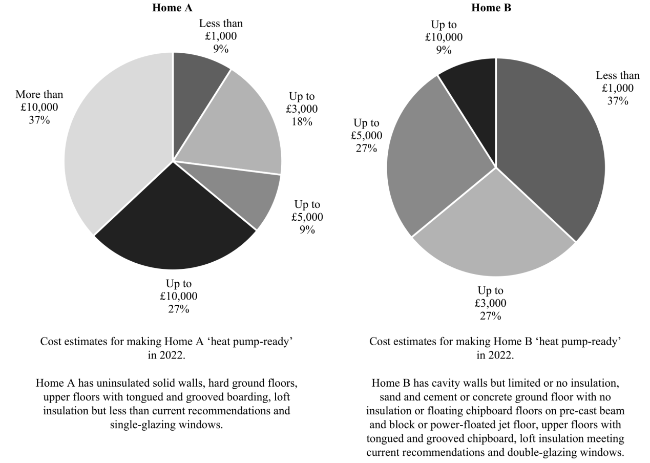

To examine this further, heat pump installation companies were then asked to give cost estimates of retrofitting two home archetypes to make them heat pump-ready to achieve good efficiency performance, as illustrated in Fig. 2. The two archetypes were developed using the University of the West England’s Construction Website, created by the Centre for Architecture and Built Environment’s Educational Resources for the Built Environment programme [129]. The first home archetype is representative of an older, period property, typical of homes built before 1920s. The second home archetype is representative of a newer property, typical of homes built after building regulations were introduced for the first time.

Fig. 2 Estimated costs to make Home A and B heat pump-ready according to heat pump installation companies |

1.27 Perspectives on approaches to meeting market needs

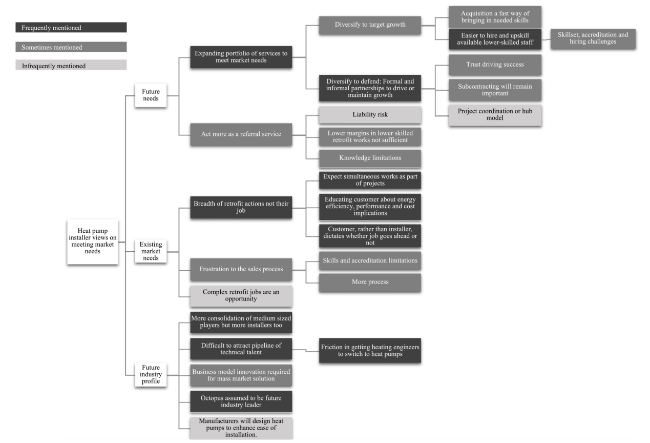

Figure 3 outlines the answers and themes derived from the heat pump installation company interview regarding their current and future approaches to meeting the market’s needs. Emerging themes have been coded and shaded, with darker shades denoting stronger, more consistent commentary across the respondents.

Fig. 3 Themes from the content analysis of heat pump installer views on meeting market needs |

Respondents generally saw that the services offered by their company would need to change over time. For example, a clear majority of heat pump installation companies said that if a home was not heat pump-ready it was currently not their job to make it so, however they believed they would need to expand their portfolio of services in the next five years to fill this gap. This indicates a broad acknowledgement that business models may need to adapt to be competitive as the market grows. Only one respondent said they would keep to pure installations.

Of those that said they would expand their services, four said they would do this by hiring or training existing staff while two larger players said they would undertake mergers and acquisitions to achieve necessary growth. A challenge highlighted - irrespective of likely expansion method - was the breadth of work needed and the incompatibility of high-skilled in-demand engineers to deliver lower skilled retrofit tasks. Accreditation barriers were also raised. These factors were underpinned by an overwhelming concern of how the industry would develop a skilled workforce to meet future demand. Of those who said they would establish partnerships, some said they would look to develop existing informal arrangements while others would strike up formal partnerships. A trusted network was deemed critical in all cases.

In terms of how this expansion would contribute towards revenue and profit, respondents were more cautious. Many respondents saw business model adaptation as a prerequisite to maintaining their heat pump installation demand. But respondents said that most retrofit works would be delivered at a lower margin than heat pump installations. There was acknowledgement that there is customer value in being a one-stop-shop service, and therefore the potential to charge a premium. But this view was tempered by a view that doing a breadth of retrofit works was fraught with risk if any part goes wrong.

Finally, on the likely industry dynamics in 5 years’ time, most said there would be a higher volume of ‘one-man-band’ installation companies, but that some consolidation of medium players was likely because of relative market fragmentation today. Almost all respondents cited a single energy supplier as the most likely player to deliver business model innovation and succeed in targeting the volume market9(9 The volume market refers to the mass market of homeowners that need to switch from gas to electrified heat over time.) with packaged solutions. Heat-as-a-service (“HaaS”) was also raised as opportunity for removing upfront costs and incentivising the transition to lower carbon heating. HaaS would see homeowners agreeing a contract with an energy service contracting organisation (ESCO). The ESCO would agree to deliver a specified level of energy performance (e.g. 21ºC internal temperature) through home improvements and a new heating system in exchange for a monthly fee for a fixed period of time.

1.28 Perspectives on appropriateness of government action

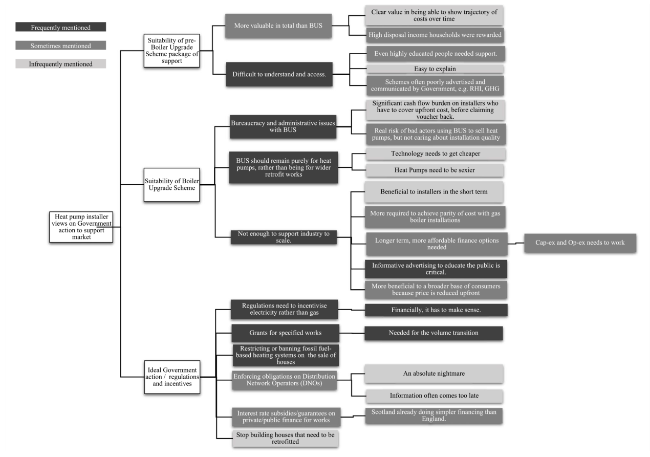

Figure 4 outlines the headline answers and themes derived from installation companies views on the Government’s action to support the market

Fig. 4 outlines the headline answers and themes derived from installation companies views on the Government’s action to support the market |

Almost all heat pump installation companies were overwhelmingly in favour of regulations and incentive schemes designed to drive adoption of heat pumps, but there was divergence on which approach was best. There was near uniformity on the need for Government to reduce the cost of electricity relative to gas to reduce the running costs of heat pumps compared to fossil gas boilers, something not widely explored in previous studies. Secondly, although grants for specified works were picked second most, many respondents felt the Boiler Upgrade Scheme was insufficient in scale to hit the Government’s targets, and major concerns were raised about Government and Ofgem’s capacity to deliver a well-functioning scheme. Restricting or banning fossil fuel-based heating systems on the sale of homes was the third most chosen measure but deemed least likely to happen. More obligations on Distribution Network Operators (DNOs) to provide the network upgrades necessary to enable heat pump installation and their connections to the grid was often highlighted as critical. Installers commented that DNOs tended to overcalculate the additional capacity required for a heat pump installation and therefore disrupt the customer journey by rejecting applications for upgrades. Interest rate subsidies or guarantees on finance for works were also popular, with several respondents citing Scotland’s low-cost loans as a solution to encouraging retrofit works and heat pump installations. As noted in the literature review of previous schemes, the Green Deal finance costs were seen as too expensive and the Renewable Heat Incentive only benefited wealthier home owners who could afford upfront costs.

Almost all heat pump installation companies said the Government’s package of support to promote energy efficiency and low carbon heating prior to the Boiler Upgrade Scheme was difficult for households to understand and access. Despite having educated customers, most heat pump installation companies indicated they needed line-by-line explanations of how to apply for schemes.

Factoring in the Boiler Upgrade Scheme, all heat pump installation companies felt Government was not doing enough to support the industry. Although heat pump installation companies viewed the Boiler Upgrade Scheme as better than nothing, they felt underlying issues were preventing the volume market from switching to low-carbon heating. The interviewees argued that heat pumps needed to achieve cost parity with gas boilers and more was needed to mitigate both upfront and operational costs too. Heat pump installation companies highlighted that electricity needs to be cheaper to purchase relative to carbon-emitting fossil fuels such as gas, or gas more expensive. There was also a widely held view not expressed in the literature that Government needs to do more to educate the public about the transition to low-carbon heating as part of promoting schemes. The frequency of new schemes and publicity regarding those that were seen to have failed contributed to this view.

Despite generally negative sentiment on its configuration and potential impact, it was acknowledged that the Boiler Upgrade Scheme funds heat pumps upfront and therefore reduces costs to homeowners, a noticeably different approach to the Renewable Heat Incentive. Finally, despite heat pump installation companies overwhelmingly favouring a fabric-first approach to installing heat pumps, most felt the Boiler Upgrade Scheme vouchers should only be used for heat pumps rather than contributing to building upgrades that may help heat pump performance.

1.29 Summary

In summary, heat pump installation companies highlighted the uneven playing field for heat pumps in comparison to gas boilers - particularly around achieving running cost parity - and that it would be vital for the government to rectify this for homeowners to begin making the switch. Further, heat pump installation companies argued that a critical part of this process should be educating the public on lower carbon heating and doing a better job of advertising new incentive schemes to homeowners. Despite relative clarity on what the government should do, this was contrasted by inconsistent views on the types of business models and solutions could work for the volume market.

1.30 A nationally representative public opinion survey on heat pump adoption and readiness

The final method was a nationally representative survey of 2,000 adults in Britain to provide a homeowner’s perspective on the transition to lower carbon heating using heat pumps. Pre-qualification questions were used to identify homeowners in England with gas boilers. The results are split into four sections: likeliness (intention) to transition to lower carbon heating; awareness of what home improvements are needed to undertake the transition; willingness to spend on the transition, and concern factors regarding the transition. Simple and linear regressions were run to test hypotheses in relation to both income and age with respect to the likeliness to transition to lower carbon heating, awareness of necessary home improvements to make homes heat pump-ready, and willingness to spend on home improvements to make homes heat pump-ready. In all cases, the relationships were weak. These regressions are available in the support materials.

1.31 Likeliness (intention) to transition to lower carbon heating

The first area of investigation looked at the likelihood of homeowners to upgrade their home to run on a lower carbon heating system in future. 22% were likely (defined as likely and extremely likely) and 50% unlikely (defined as unlikely and extremely unlikely) to do so, as outlined in Table 6.

Table 6 How likely are you to upgrade your home to run on a lower-carbon heating system in the next 5 years? (e.g. using a heat pump to heat your home) |

| n | % | |

|---|---|---|

| Likely | 219 | 22% |

| Neutral | 185 | 18% |

| Unlikely | 519 | 50% |

| Don’t know | 107 | 10% |

1.32 Awareness of home improvements needed for the transition

Asked about their awareness of what was necessary to make their home heat pump-ready, 89% had low or no awareness, as highlighted in Table 7.

Table 7 Do you have an understanding of the types of work that may be required to make your house heat pump-ready? |

| N | % | |

|---|---|---|

| Higher awareness | 110 | 11% |

| Low or no awareness | 774 | 89% |

Further, asked if they believed their home met the Boiler Upgrade Scheme’s eligibility criteria, there was a mixed response, as shown in Table 8. 35% declared their home was likely to meet the criteria. Comparing this with the results of the first method, this suggests a knowledge gap between homeowners (35% think their home is likely to meet the criteria) and the 50% of England’s homes estimated to be Boiler Upgrade Scheme-eligible.

Table 8 Do you (think you) meet the Boiler Upgrade Scheme’s eligibility criteria? |

| N | % | |

|---|---|---|

| Likely | 359 | 35% |

| Neutral | 154 | 15% |

| Unlikely | 316 | 31% |

| Don’t know | 202 | 20% |

1.33 Willingness to spend on the transition

Homeowners were then asked about the types of home improvements they would not consider to make their home heat pump-ready, as outlined in Table 9. To prevent influencing their choices, respondents were not provided cost estimates of respective home improvements. Encouragingly, 37% of respondents would at least consider all the home improvements. Nearly 90% would consider air sealing, loft insulation, improved glazing, and forms of wall insulation - measures regarded as important during the heat pump installation company interviews. However, only 58% would consider installing underfloor heating - considered an important home improvement for enhanced heat pump performance in the literature review.

Table 9 Please select the home improvements you would NOT be willing to consider or implement |

| n | % | |

|---|---|---|

| Installing underfloor heating | 434 | 42% |

| Replacing heating pipework | 290 | 28% |

| Floor insulation | 263 | 26% |

| Replacing radiators | 244 | 24% |

| Cavity Wall Insulation or Solid Wall Insulation | 189 | 18% |

| Installing a smart meter | 184 | 18% |

| Double or triple glazing | 129 | 13% |

| Loft insulation | 119 | 12% |

| Air sealing / draught proofing | 118 | 11% |

| None of these / I will consider making all improvements | 379 | 37% |

Respondents were then asked to consider how much they would be willing to spend on home improvements to make their homes heat pump-ready, as shown in Table 10. Significantly, 57% said they would not do any home improvements unless they are funded by Government. In addition, nearly 1 in 5 (18%) people said they would not spend more than £1,000 on works to make their home heat pump-ready.

Table 10 What is the maximum cost you would be willing to incur to ensure your home is heat pump-ready? |

| N | % | |

|---|---|---|

| I wouldn’t - it is not a priority unless it is fully funded by Government | 585 | 57% |

| < £1,000 | 181 | 18% |

| < £3,000 | 148 | 14% |

| < £5,000 | 81 | 8% |

| < £10,000 | 30 | 3% |

| < £20,000 | 5 | 1% |

1.34 Concern factors regarding the transition

Finally, respondents were asked separately about their levels of concern regarding aspects of transitioning to lower carbon heating, as shown in Table 11. These factors were identified through the literature review and the heat pump installation company interviews. When asked how concerned homeowners were about certain aspects of transitioning to low carbon heating, 70% of respondents selected upfront costs and 52% selected future energy bills. Equally, this corresponds with the view expressed by heat pump installation companies that until electricity costs came down and the cost of gas for heating was disincentivised, concern about the transition would remain.

Table 11 How concerned are you about the following aspects of transitioning to a lower-carbon heating system? |

| Upfront costs | Future energy bills | Disruption | Warmth worry | |||||

|---|---|---|---|---|---|---|---|---|

| n | % | n | % | n | % | n | % | |

| More concerned | 717 | 70% | 301 | 52% | 495 | 48% | 399 | 39% |

| Less concerned | 312 | 30% | 280 | 48% | 535 | 52% | 631 | 61% |

1.35 Summary

Evidence from this method indicates low intention to decarbonise among homeowners - only 22% are likely or very likely to upgrade their home to run on a lower carbon heating system in the next five years. Fewer homeowners think they are eligible for the Boiler Upgrade Scheme than estimated in the first method (35% vs 50%). A concern is that 89% of homeowners had little or no awareness that home improvements might be needed to make their home heat pump-ready, particularly given the results from the previous methods showing that only 10% of homes are heat pump-ready. This high-need low-awareness dynamic illustrates the low base England is starting from to successfully decarbonise its housing stock.